News

Iron ore prices rose by nearly 7% in March amid supply risks

Tweet

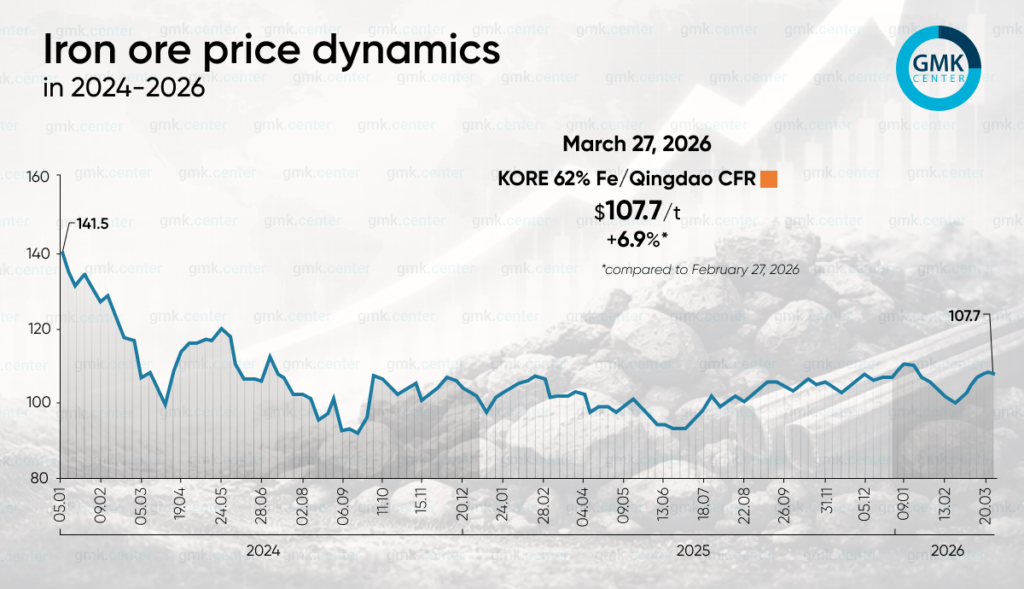

Iron ore prices rose by 6.9% during the period from February 27 to March 27, 2026, reaching $107.74/t CFR (KORE 62% Fe/Qingdao). The average price for the raw material in March was $106.33/t, compared to $101.53/t in February. Thus, the market recouped some of its previous losses and returned to levels around $108/t CFR over the course of the month.

In the first half of March, the market was supported primarily by supply concerns. Key drivers included restrictions on BHP’s shipments to China, uncertainty surrounding imports of certain cargoes, and the risk of disruptions in Australia. High freight costs and expectations that Chinese steelmakers would restock following the gradual lifting of temporary production restrictions provided additional support. China’s government guidance of 4.5–5% GDP growth for 2026 also added some optimism, supporting expectations for demand for steel and raw materials.

At the same time, the market remained highly sensitive to news developments. As early as March 16–18, prices fluctuated due to easing concerns over a shortage of BHP raw materials and weak fundamental demand indicators. The start of the peak construction season in China was sluggish, steelmakers’ margins remained low, and pig iron output did not show steady growth. Steel mills largely adhered to a procurement strategy without actively building inventories, which limited the potential for ore price increases.

Toward the end of the month, external macroeconomic and geopolitical factors further influenced market dynamics. The conflict surrounding Iran supported energy and logistics costs, providing cost-based support for seaborne shipments. In addition, tense negotiations between China Mineral Resources Group and major suppliers, primarily BHP, created a local shortage of certain ore grades in the spot market, even despite generally high stockpiles in Chinese ports.

Weather-related risks in Australia emerged as a separate driver. In late March, the threat of Cyclone Narelle and the temporary closure of several ports in the Pilbara region briefly pushed prices higher. However, once the extent of the disruptions proved to be limited, the market partially retreated. On March 25, environmental restrictions on steel production in Hebei Province created additional pressure, dampening expectations for raw material consumption.

In the short term, the iron ore market is likely to remain volatile within a range close to current levels. Prices will be supported by risks of supply disruptions, high energy costs, and the gradual recovery of pig iron production in China. At the same time, high port inventories, weak margins for steelmakers, and cautious purchasing by mills will limit further growth.

Source: GMK Center

Tweet

Related News

- Brazil and China should cooperate in the field of environmentally friendly steel: study

- Germany increased steel production by 4.8% y/y in February

- Global high-grade iron ore market is set to grow

- Global iron ore exports rise modestly in CY'25 as Brazil drives growth

- China expands restrictions on iron ore imports from BHP

- Germany - Trimet Aluminium’s Essen foundry reaches 10 million tonnes aluminium casting milestone

- Here's the Top 15 List of Pig Iron Companies 2026

- Poland - Targi Kielce Industrial Autumn – the Central and Eastern Europe’s industry’s focal point

- See all News