News

India: Iron foundry industry trends strengthen in FY'26, grey iron retains dominance

Tweet

- Grey iron anchors volumes while SG iron gains structural importance

- Automotive and infrastructure remain primary demand drivers

- Product mix reflects gradual shift toward value-added castings

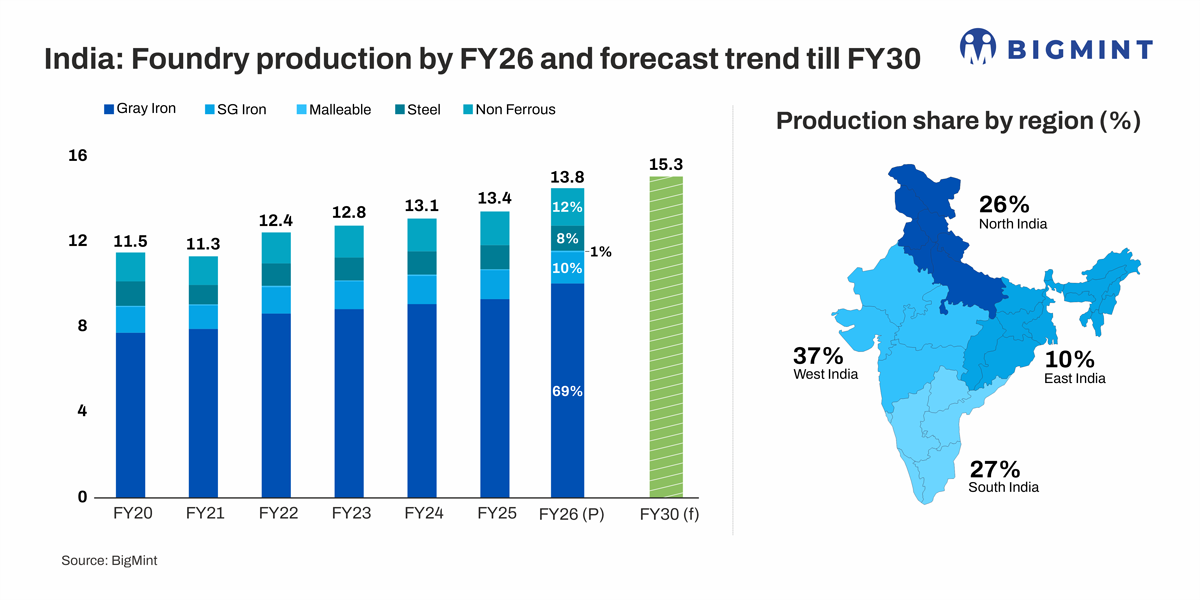

India's iron casting market in FY'26 continues to show steady expansion, supported by resilient domestic demand from automotive, infrastructure, and industrial machinery segments. As per provisional data, total casting output for FY'26 is estimated at around 13.8 million tonnes (mnt). This reflects stable capacity utilisation across major foundry clusters despite export-related challenges in select regions.

Product trends

Grey iron remains the backbone of India's casting industry, accounting for 69% of total output in FY'26. Its dominance is underpinned by sustained demand from engine blocks, brake components, pipes, and agricultural machinery, where cost efficiency and machinability remain critical.

SG iron constitutes 10% of production, with volumes gradually rising as OEMs increasingly prefer higher strength-to-weight components, particularly in automotive, railways, and infrastructure applications. Industry participants noted that SG iron adoption is accelerating in safety-critical and load-bearing components, reflecting a slow but structural upgrade in product quality.

Steel castings account for 8%, largely driven by heavy engineering, power equipment, and defence-related orders, while malleable iron remains marginal at 1%, constrained by substitution from SG iron.

Non-ferrous castings form a significant 12% share, supported by aluminium and copper alloy demand for automotive light weighting, electrical equipment, and renewable energy segments.

Regional market dynamics

Indias iron casting capacity in FY'26 is estimated at 13.8 mnt, with production clustered around key industrial belts. West India dominates with 37% share, or about 5.11 mnt, supported by strong automotive, tractor, and engineering ecosystems in Maharashtra and Gujarat. Better access to organised scrap yards, ports, and OEM-linked demand continues to support higher operating rates and relatively stable margins in the region.

South India accounts for 27% of capacity at around 3.73 mnt, anchored by export-oriented foundries in Tamil Nadu, Karnataka, and Andhra Pradesh. The region has a higher concentration of technologically advanced units producing value-added grey and SG iron castings for automotive and industrial machinery applications, helping offset volatility in export demand.

North India holds 26% share, equivalent to 3.59 mnt, driven largely by demand from tractors, construction equipment, and agricultural machinery. However, industry participants note that foundries in the region remain more exposed to scrap price fluctuations and freight costs, leading to cautious procurement and tighter working capital management.

East India contributes around 10% of capacity, or 1.38 mnt, benefiting from proximity to raw material sources and legacy heavy-engineering customers. Smaller plant sizes, higher dependence on exports, and recent global trade disruptions continue to cap utilisation levels in the region.

Demand trends

Automotive remained the largest demand driver for Indian foundry mills in FY'26, absorbing the bulk of grey and SG iron output for engine blocks, brake components, suspension, and drivetrain parts. While volume demand has stayed stable, OEM price discipline has kept margins under pressure, pushing foundries to focus on yield optimisation and higher SG iron penetration.

Infrastructure, construction, and industrial machinery form the second key demand pillar, led by pipes, valves, manhole covers, and capital goods castings. Government-led capex has supported steady base-load demand, while export-oriented applications have softened amid global trade disruptions, prompting foundry mills to prioritise domestic end-use segments to stabilise utilisation.

Structural and trade shifts

Indian foundry clusters witnessed gradual structural shifts in FY26, with increased focus on technology upgrades, automation, and quality compliance, particularly in western and southern India. Several mid-sized foundries across Kolhapur, Coimbatore, Kolhapur-Sangli belt, and KolhapurBelgaum corridor initiated investments in moulding lines, sand reclamation systems, and energy-efficient furnaces to improve yields and meet tighter OEM specifications.

Export-oriented clusters, especially in Coimbatore and Kolhapur, faced softer order flows following global trade disruptions and higher tariffs in key markets such as the US. This prompted many units to rebalance toward domestic automotive, tractor, and infrastructure-linked demand, while selectively reducing exposure to low-margin export orders.

Sustainability and compliance also gained prominence, with foundries increasingly aligning operations with ESG norms, emission controls, and scrap traceability requirements. Industry participants noted that clusters with better access to organised scrap and logistics continued to maintain higher utilisation, while smaller units in eastern India remained more vulnerable to demand volatility and working capital stress.

BigMint foundry-grade scrap prices by region

Price trajectory

Foundry-grade scrap prices moved higher across key regions in January, supported by steady foundry offtake and tighter prompt availability. In Kolhapur, CR busheling (low Mn, bundled) was assessed at INR 39,500/t, up INR 300/t w-o-w, while plate cutting scrap (LS & LP, loose) rose to INR 36,500/t. Demand from grey and SG iron foundries remained stable, with purchases largely need-based.

In Chennai, stronger buying interest pushed prices higher, with CR busheling rising INR 500/t w-o-w to INR 39,250/t and plate cutting scrap increasing to INR 36,200/t. Limited spot availability and higher replacement costs supported the uptrend.

Eastern India saw the sharpest rise, as Kolkata plate cutting scrap jumped INR 1,000/t w-o-w to INR 37,000/t, driven by restocking and reduced local supply. Overall, western and southern markets continued to command a premium, reflecting higher operating rates and stronger scrap absorption in FY26.

Outlook

Toward FY'30, Indias casting mix is expected to gradually shift toward higher SG iron and non-ferrous share, though grey iron will remain dominant in volume terms. Capacity additions, automation, and quality upgrades will be key to sustaining competitiveness.

Source: Bigmint

Tweet

Related News

- Brazil and China should cooperate in the field of environmentally friendly steel: study

- Germany increased steel production by 4.8% y/y in February

- Global high-grade iron ore market is set to grow

- Global iron ore exports rise modestly in CY'25 as Brazil drives growth

- Iron ore prices rose by nearly 7% in March amid supply risks

- China expands restrictions on iron ore imports from BHP

- Germany - Trimet Aluminium’s Essen foundry reaches 10 million tonnes aluminium casting milestone

- Here's the Top 15 List of Pig Iron Companies 2026

- See all News