News

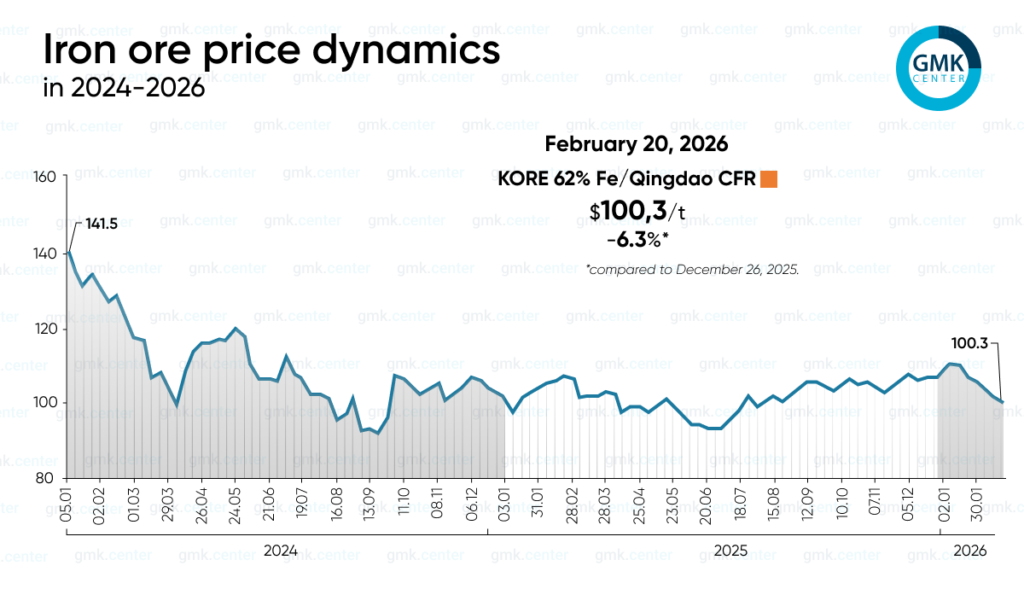

Iron ore prices have fallen by more than 6% since the beginning of the year

Tweet

Currently, Qingdao (KORE 62% Fe) quotes are at their lowest level since August 2025

Prices for Qingdao iron ore (KORE 62% Fe) fell by 6.3% to $100.26/t CFR between December 26, 2025, and February 20, 2026. Currently, quotations are at their lowest level since August 2025.

At the beginning of 2026, the iron ore market was influenced by a combination of seasonal and fundamental factors that gradually shifted the balance toward excess supply. Although prices attempted to stabilize at the end of January due to pre-holiday restocking by Chinese steelmakers ahead of the Lunar New Year, this effect proved to be short-lived.

In the second half of January, prices were temporarily supported by purchases from steel mills, which were building up stocks to ensure continuous operation during the holidays. Futures markets and rising coking coal prices were additional factors for optimism. However, even during this period, statistics showed a deterioration in fundamental indicators: steel inventories at plants grew, and construction activity declined due to weather conditions and the seasonal slowdown.

By the end of January, support from restocking began to run out. Steel producers limited purchases due to weak margins and cautious financial policies, while port ore stocks in China approached multi-year highs. Additional pressure came from expectations of environmental restrictions and a slower-than-expected recovery in pig iron production.

In early February, the market entered a downward phase. After the pre-holiday purchasing season ended, demand fell sharply, while supply remained high. Even weather risks in Australia and temporary supply disruptions failed to support prices, as excess inventories offset any shortages. At the same time, new shipments of high-quality ore from the Simandou project began to arrive, reinforcing expectations of global supply growth in the medium term.

During the holiday period, liquidity fell sharply, traders closed their positions, and futures continued to weaken. Low demand from Chinese steelmakers remained a key market factor.

After the holidays in China, a short technical recovery in prices is possible due to the return of mills to purchasing. However, fundamentally, the market remains in a negative phase, as high inventories, weak construction activity, and a gradual increase in supplies (particularly from Simandou) will limit growth potential. In the coming months, prices are likely to fluctuate around or slightly above $95-105/t CFR, with the risk of further declines in the event of weak steel demand in China.

Source: GMK Center

Tweet

Related News

- Brazil and China should cooperate in the field of environmentally friendly steel: study

- Germany increased steel production by 4.8% y/y in February

- Global high-grade iron ore market is set to grow

- Global iron ore exports rise modestly in CY'25 as Brazil drives growth

- Iron ore prices rose by nearly 7% in March amid supply risks

- China expands restrictions on iron ore imports from BHP

- Germany - Trimet Aluminium’s Essen foundry reaches 10 million tonnes aluminium casting milestone

- Here's the Top 15 List of Pig Iron Companies 2026

- See all News